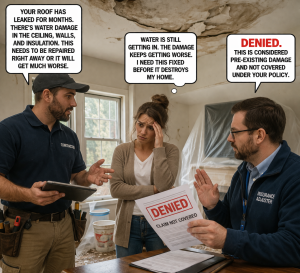

When the Insurance Company Won’t “Approve” Repairs — But Might Deny Them Later

When a property is damaged, homeowners are often caught between three competing pressures: a contractor recommending necessary repairs, worsening conditions that demand immediate action, and an insurance company refusing to approve or cover the work. This creates a high-risk situation where making the wrong decision can lead to significant out-of-pocket costs.

The key challenge is that insurance carriers often avoid “authorizing” repairs, yet may later deny payment for work they believe was unnecessary or not covered. Meanwhile, delaying action can result in additional damage that may not be reimbursed if it’s deemed preventable.

To navigate this, property owners must balance urgency with documentation and clarity. Critical decisions should focus on preventing further damage, clearly separating emergency mitigation from permanent repairs, and maintaining thorough records of all conditions, communications, and contractor recommendations.

Professional representation plays an important role in this process. Having an advocate who understands policy language, claim procedures, and documentation standards helps ensure decisions are made strategically—not reactively—reducing the risk of denied coverage and unexpected financial exposure.

{kind=link}

{kind=link}

{kind=link}