House Bill 1972 and Its Companion Senate Bill: A Closer Look

Two new bills introduced in the Pennsylvania General Assembly—House Bill 1972 and its companion Senate Bill—seek to dramatically alter the landscape of public insurance adjusting in Pennsylvania. While presented as consumer protection measures, these proposals could instead cripple the ability of licensed public adjusters to assist homeowners and small business owners in recovering fair insurance settlements after property losses.

What the Bills Propose

House Bill 1972 would amend the Public Adjuster Licensing Law of 1983 by imposing a series of more restrictive measures that can reduce the professional’s ability to operate. Among the most significant provisions are:

- Fee Caps: A hard ceiling of 15% on all claims—and just 10% on catastrophic losses—regardless of the size, complexity, or costs involved in handling the claim

- Lengthy Right of Rescission: A 15-business-day rescission period (triple the length allowed in nearly any comparable industry) that introduces long delays, uncertainty, and lost capacity for legitimate representation

- Prohibitions on Business Ownership: Public adjusters would be barred from having any financial interest in a construction, restoration, or repair company, even if those entities are legally separate or serve other clients

- Referral and Compensation Restrictions: The bill would make it illegal for a contractor to pay, refer, or even collaborate with a public adjuster—essentially outlawing any working relationship between the two professions

- Increased Bonding Requirements: The mandatory bond amount for adjusters would double from $20,000 to $40,000, further raising barriers for small firms and independent professionals

How This Impacts Policyholders

For property owners—homeowners, churches, and small businesses—these bills would have devastating consequences.

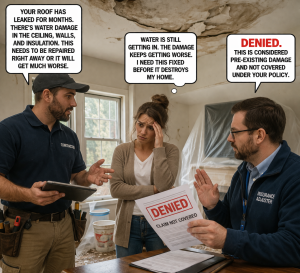

Public adjusters serve a crucial consumer-protection role: they represent insureds, not insurance companies. By limiting how adjusters can work and how they are compensated, these bills tilt the balance of power even further toward insurers.

If enacted:

- Many small adjusting firms could close, leaving vast portions of the state without access to licensed representation.

- Property owners could face longer delays and less competition in claim representation, leading to smaller settlements.

- Consumers could have fewer options to challenge underpaid claims, as legal costs often exceed disputed claim amounts, making litigation impractical.

- Catastrophe victims could be particularly harmed, as 10% caps may not sustain the travel, documentation, and expert costs necessary in large-loss claims.

A Step Backward for Consumer Rights

The proposed bills appear to stem from pressure by the insurance industry, which has long sought to limit the presence of licensed public adjusters in the claim process.

Yet, the stated goal of “protecting consumers” could be contradicted by the real-world effect: these measures would eliminate professional advocates who ensure claim accuracy, fair market repair pricing, and compliance with policy terms.

Unlike insurance company adjusters—who are salaried by the insurer—a public adjuster is the only licensed professional legally authorized to represent the policyholder’s interests in a property damage claim. Weakening this profession harms not just the adjusters, but the thousands of Pennsylvania families and businesses they serve each year.

What You Can Do

Industry professionals, policyholders, and consumer advocates are urged to:

- Contact your State Representative and Senator to oppose HB 1972 and its companion bill.

- Join advocacy organizations such as the Heartland Association of Public Insurance Adjusters (HAPIA) to stay informed and participate in coordinated outreach.

- Share your story of how a public adjuster helped you or your clients recover fairly after a loss. Lawmakers need to hear the human side of these policy decisions.

Final Thought

House Bill 1972 represents more than just a policy debate—it is a fundamental question about who gets to stand beside the policyholder when disaster strikes. Public adjusters have earned their place as a vital consumer safeguard. Restricting their ability to operate would leave Pennsylvanians to face insurance companies alone—precisely when they need help the most.

{kind=link}

{kind=link}

{kind=link}