Estimated reading time: 7 minutes

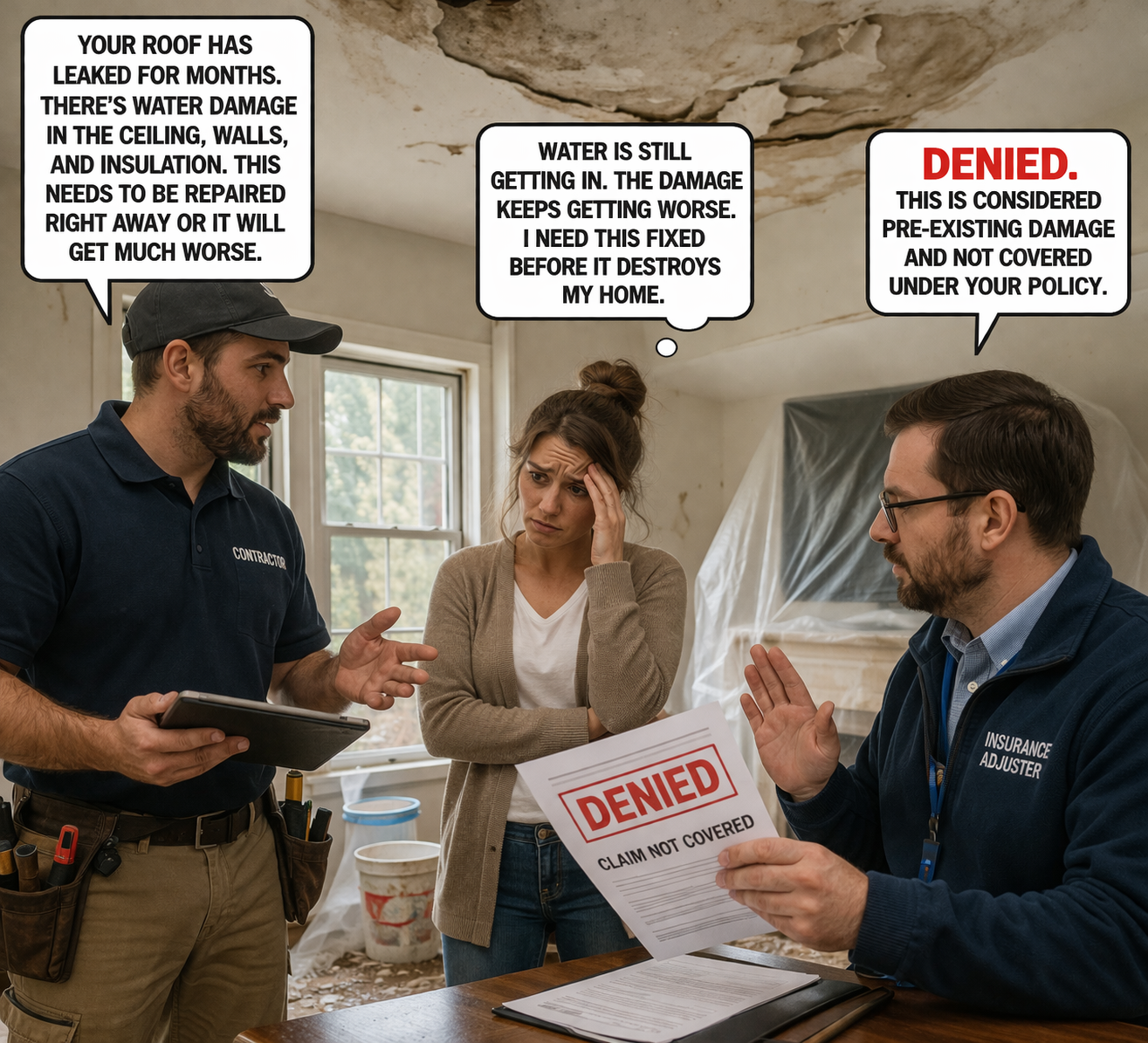

One of the most frustrating positions a policyholder can find themselves in is this:

You have a contractor telling you what needs to be repaired.

You have ongoing damage or urgency pushing you to act.

And you have an insurance adjuster saying:

“We can’t approve your repairs.”

At the same time, that same claim may later result in:

“We are denying that portion of the work.”

So what are you supposed to do?

This gray area creates real financial risk for property owners—especially on larger or more complex losses where scope, code compliance, and structural integrity are still being evaluated.

Let’s break this down clearly.

Why This Happens

Insurance companies often avoid using the word “approve” because they are not a party to your construction contract and they do not want to be seen as directing repairs. While this may help the insurance company limit liability for construction outcomes, it is not helpful for the policyholder (you) when it comes time to make a financial choice.

In practice, adjusters do make scope and pricing determinations frequently and those decisions directly impact what gets paid. That leaves policyholders stuck in the middle. Often stuck between two bad options:

- Move forward → risk non-payment

- Wait → risk worsening damage or delays (that can result in nonpayment)

The Real Risk: You Become the Decision-Maker

When you proceed without clear alignment, you may authorize work that exceeds policy scope which could make you personally responsible for gaps in payment.

Another risk… you may initiate code upgrades not yet triggered or validated during the claims coverage investigation process. Without confirmation of building code coverage, many policyholders have made a costly mistake that had to be paid out-of-pocket as it was later determined outside of the reasonable repair scope.

This is especially critical in:

- Structural damage (tree impact, fire, collapse)

- Older buildings with code issues (like pre-1900 homes)

- Commercial properties with larger financial exposure

Top 3 Recommendations for Navigating These Decisions

1. Separate “Emergency Mitigation” from “Full Repairs”

Not all work carries the same level of risk.

In residential construction, unless specifically defined by the insurance policy, emergency mitigation refers to the immediate, proactive, and often mandatory actions taken to prevent further damage to a home, protect occupants, and stabilize the structure after a disaster or unexpected incident. It is the essential “damage control” phase that happens right after an emergency—such as a flood, fire, windstorm, or severe pipe burst—to prevent minor damage from becoming major, costlier destruction.

In commercial construction, unless defined by the insurance policy, emergency mitigation typically refers to the ongoing, sustained effort to reduce the loss of life and property damage from disasters by minimizing their impact. It involves proactive measures like land use planning, retrofitting buildings, and enforcement of safety codes to reduce long-term risk before hazards occur.

Very different concepts.

And when contemplating initiating emergency mitigation efforts to lessen the potential for further damage and/or the loss of life, where can the line for work authorization be safely drawn?

Emergency Mitigation (Generally Safe to Proceed):

- Tarping

- Water extraction

- Temporary stabilization

- Preventing further damage

These actions are typically covered under your insurance policy requirements duty to mitigate damages. In Ohio, insured individuals have a legal duty to take reasonable, practical steps to minimize losses following an insurance-covered event, known as the duty to mitigate damages. Failure to do so can result in the insurance company denying or reducing coverage for the additional, avoidable damages.

Full Repairs (Higher Risk):

- Full roof replacement decisions

- Structural rebuilds

- Code upgrades

- Finish materials and scope expansions

👉 Recommendation:

Move forward with mitigation—but slow down major repair decisions until scope alignment is clearer. The insurance adjuster will never tell you not to perform work you deem necessary to repair your property. At most, they may caution or send a Reservation of Rights (ROR) letter to limit their liability during this period.

2. Force Scope Clarity in Writing (Before You Commit)

If the adjuster won’t “approve,” you can still demand position clarity. Ask direct, written questions like:

- “Do you dispute that this damage is related to the loss?”

- “Which specific line items are not being considered at this time?”

- “What additional documentation is needed to evaluate this scope?”

This does two things – it creates a documented history for your personal file (and their claim file) as well as locking in the carrier’s position. In an environment where claims adjusters are often reassigned due to case complexity or simply changed due to staffing changes, you’ll want a record of any specific conversations you relied upon for your decision. It’s a great negotiation resource and it can also be evidence of mishandling if the issue must be escalated.

👉 Rule of Thumb:

Never rely on verbal conversations when making six-figure decisions.

If it’s not in writing, it doesn’t protect you.

3. Align Your Contractor Scope With a Defensible Claim Strategy

Contractors often write estimates based on what it takes to do the job correctly. Scope definition in property estimating is the detailed documentation of all work, materials, and services required for a construction or repair project, outlining specific inclusions, exclusions, and clarifications. A well-defined scope acts as a baseline to ensure accurate cost estimates, preventing budget overruns and scope creep by clearly defining the “what” and “how” of the project.

Insurance carriers evaluate repairs estimates based on:

- Policy language – the terms and conditions of your policy contract

- Causation – the active (or dominant) cause of the property damage

- Scope limitations – the detailed evaluation of all recommended, related repairs

- Pricing frameworks – market pricing vs competitive bids for related materials and labor cost

Those are not always the same thing.

👉 Recommendation:

Before proceeding, reconcile the contractor estimate against the insurance company estimate to identify disputed vs. undisputed (agreed upon) scope. Schedule the work in phases if necessary to allow time to obtain the necessary reliance.

Example approach:

- Phase 1: Stabilization (emergency mitigation) + undisputed repairs

- Phase 2: Disputed items (pending review by the insurance company)

This protects cash flow for any monies already issued by the adjuster and it reduces out-of-pocket exposure for disputed repairs down the line.

Where a Public Adjuster Changes the Outcome

And unfortunately, this is exactly where most policyholders get into trouble. They are forced to make technical, financial, and legal decisions at the same time but without guidance.

A licensed public adjuster steps in to:

1. Define and Defend Scope Before You Build It

- Evaluates full damage (not just visible issues) and executes your Duties After A Loss with a Proof of Loss, as determined by the policy requirements. See the Ohio Administrative Code for a definition of the Proof of Loss and its submission requirements in the state.

- Works with your contractor to identify structural and system-wide impacts and obtain the necessary evidence for submission to the insurance company

- Aligns scope in accordance with available policy coverages

2. Control the Timing of Decisions

- Helps you avoid premature commitments

- Advises when to proceed vs. pause (if allowed under state regulations)

- Coordinates mitigation vs. reconstruction strategy with your chosen contractors

3. Reduce Your Financial Risk

- Separates what is likely payable vs. disputed allowing you to make better decisions

- Builds documentation before work begins, where possible

- Negotiates scope with the adjuster so you’re not funding gaps

4. Create Leverage With the Carrier

- Forces clearer positions from the insurance company

- Prepares the file for escalation (appraisal or legal if needed)

- Rebuts “after-the-fact” denials vs allowing them to go unchallenged

The Bottom Line

If you hear:

“We can’t approve your repairs…”

You should immediately be thinking:

- What parts of this scope (estimate) are actually in dispute?

- What am I financially exposed to if I proceed?

- Do I have enough documentation to defend this decision later?

Because once the work is completed, your leverage decreases significantly.

Final Thought

The hardest part of a property claim isn’t always identifying the damage—it’s making the right decisions before the claim is fully resolved.

And in the absence of clear direction, the burden shifts to the policyholder.

You don’t have to carry that alone.

Disclaimer: Green Public Insurance Adjusting are not attorneys and do not provide legal advice. Coverage determinations are governed by the specific terms, conditions, and exclusions of each individual insurance policy. Policyholders should consult qualified professionals when making financial or legal decisions related to their claim.

Recommended Reading:

- What Does A Public Insurance Adjuster Do — And When Should You Hire One?

- Understanding Insurance Claims After Storm Damage

- The Hidden Risk: Structural Damage from Tree Impact

- Proof Of Loss Form Submissions: One Letter That Can Decide The Fate Of An Insurance Claim

- Preparing Your Claim After You Suffer Damages

{kind=link}

{kind=link}

{kind=link}